A brief history of Mifos

(Etym. Micro Finance Open Source)

Started as an initiative of Grameen foundation, supporting more than 850,000 micro finance clients across 25+ micro finance institutions in India, Tunisia, Uganda, Kenya, Mozambique etc. Mifos is a platform built to support institutions that operate in the micro finance world. Grameen formally withdrew direct support in June 2011. Since then it has been supported by COSM, which is a diverse collective of participants building a microfinance movement powered by open source innovation. COSM aims to make microfinance more open and effective by equipping MFIs with software, collaboration tools and a local support network to use technology to reach the poor. MIFOS' mission is to create a world that can have 3 Billion Maries. This motto came about, goes the folklore, when in a visioning exercise for Mifos, wherein everyone shared their mind on how the product should shape up, one of the participant narrated the story of Marie-Claire and how he saw a world with 3 billion Maries (3 Billion being in reference to the number of people said to live on less than $2 a day).

COSM is currently in the process of re-architecting the Mifos, and building the next generation Mifos X, in the light of a lot changes -

1. In the Micro Finance's applications (Micro lending becoming more sophisticated. More product innovations to help the poor - savings, insurance

2. In regulations (Better accounting practices, governance and regulatory reporting)

3. In the platform demand - A complete inability to support and extend the current platform to manage the above

ThoughtWorks and Mifos

ThoughtWorks has worked on a few projects contributing to the extant platform, since November 2007 (Mainly from New York and Bangalore). We were one of the early contributors, through commercial implementations and contributing to the open source platform. We haven't been contributing to this platform in the past year, after Grameen's departure.

Mifos implementors global meetup (Bangalore, Oct 2012) - A diary

ThoughtWorks took part in implementing a part of their application as part of the SIP umbrella during the period 2011. MIFOS Summit happened in Bangalore during October 16-18 in which Praveena and Ram took part. The summit was mainly to focus on the current problems the users face and what are the new functionalities they look out for in the new product MIFOS X which is a complete rewrite of their existing product.

(Etym. Micro Finance Open Source)

Started as an initiative of Grameen foundation, supporting more than 850,000 micro finance clients across 25+ micro finance institutions in India, Tunisia, Uganda, Kenya, Mozambique etc. Mifos is a platform built to support institutions that operate in the micro finance world. Grameen formally withdrew direct support in June 2011. Since then it has been supported by COSM, which is a diverse collective of participants building a microfinance movement powered by open source innovation. COSM aims to make microfinance more open and effective by equipping MFIs with software, collaboration tools and a local support network to use technology to reach the poor. MIFOS' mission is to create a world that can have 3 Billion Maries. This motto came about, goes the folklore, when in a visioning exercise for Mifos, wherein everyone shared their mind on how the product should shape up, one of the participant narrated the story of Marie-Claire and how he saw a world with 3 billion Maries (3 Billion being in reference to the number of people said to live on less than $2 a day).

COSM is currently in the process of re-architecting the Mifos, and building the next generation Mifos X, in the light of a lot changes -

1. In the Micro Finance's applications (Micro lending becoming more sophisticated. More product innovations to help the poor - savings, insurance

2. In regulations (Better accounting practices, governance and regulatory reporting)

3. In the platform demand - A complete inability to support and extend the current platform to manage the above

ThoughtWorks and Mifos

ThoughtWorks has worked on a few projects contributing to the extant platform, since November 2007 (Mainly from New York and Bangalore). We were one of the early contributors, through commercial implementations and contributing to the open source platform. We haven't been contributing to this platform in the past year, after Grameen's departure.

Mifos implementors global meetup (Bangalore, Oct 2012) - A diary

ThoughtWorks took part in implementing a part of their application as part of the SIP umbrella during the period 2011. MIFOS Summit happened in Bangalore during October 16-18 in which Praveena and Ram took part. The summit was mainly to focus on the current problems the users face and what are the new functionalities they look out for in the new product MIFOS X which is a complete rewrite of their existing product.

Day 1 (Oct 16 - Visioning)

Highlights of MifosX wishlist

- New products (Savings, Insurance) and flexible micro lending products (Variable schedule, interest rates, Group loans with multiple collaterals/schedules etc)

- Accounting modules or ability to add on Accounting products

- The mobile implementation was much sought after since almost all the times the field officers end up doing repetitive work after collecting the money from the fields and doing the data entry.

- More portfolio related functionalities which typically help Micro Finance Institutions(MFI) in understanding their customer base and the overall health of their services.

- Need for infrastructure related help i.e.. Being able to spin one ec2 instance with the MIFOS platform on it instead of getting the instance and deploying all the data on it.

- Not much of product positioning or comparing with competition - the current implementors held that they adopted MIFOS after R&D on the benefits of MIFOS compared to the competition (BankersRealm and Octopus)

Day 2 (Oct 17 - Consolidating the vision for roadmap)

We spent half the day for the various teams to summarize the parallel tracks that they attended on the previous day. This was facilitated by Ed Cable, who consolidated the product bundle on the board. Followed by a prioritization among the demands on Mifos X.

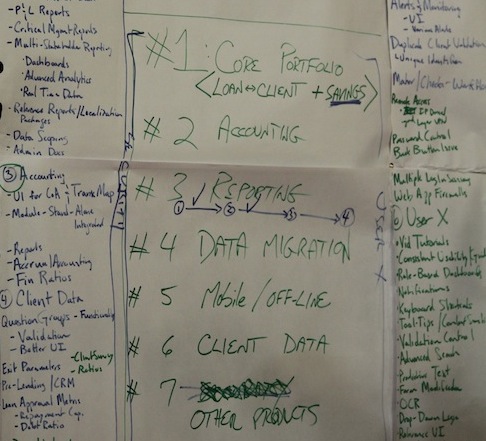

Prioritized feature buckets:

We spent half the day for the various teams to summarize the parallel tracks that they attended on the previous day. This was facilitated by Ed Cable, who consolidated the product bundle on the board. Followed by a prioritization among the demands on Mifos X.

Prioritized feature buckets:

- Core Portfolio - There was an overwhelming agreement that the current supported products in Mifos are very restrictive. Need to add Savings and make loans more flexible, at the least. These products, it has been argued are absolutely needed and in conjunction to make micro-lending, any meaningful to the poor. Hence there is an incumbent urgency on the MFI to continue to be an agent of positive change to adopt these products

- Accounting - with the increased vigilance and growing scale, Microfinance has matured its financial governance. The current Mifos platform was woefully lacking in this, probably leading to the most churn in user base

- Reporting - The MFIs are getting increasingly complex and the advent of a lot of them have also increased their need to manage their operations more intelligently. They see a need for useful information, just as any other business to monitor and improve on their operations

- Data migration from the current platform to Mifos X - the current platform has a lot of idiosyncrasies that the new one is out to change, and hence this and the volume of data poses a challenge in migration. Add to this the imperative of the existing clients to move to the new platform, makes the transition even more difficult

- Mobile/Offline data - Connectivity in a lot of places is still low. But people felt this not a huge worry

- Client data - Managing data security

- Other products - Credit Insurance, Health insurance, SHG-SHG loan...

Day 3 (Oct 18 - Field visits to Grameen Koota, Nirantara)

We set off on the final day, to see Micro finance in action at a couple of MFI's local groups in rural Karnataka. We went to a settlement close to Tumkur, a small town off 100 Kms form Bangalore, to see a women's group meetup. What followed was a great experience with a lot of learning on the real impact and impediments of Micro lending -

7:30 am - Start for Tumkur

10:00 am - Reach the settlement where Grameen Koota (GK) was meeting with the clients (neighbourhood women)

We set off on the final day, to see Micro finance in action at a couple of MFI's local groups in rural Karnataka. We went to a settlement close to Tumkur, a small town off 100 Kms form Bangalore, to see a women's group meetup. What followed was a great experience with a lot of learning on the real impact and impediments of Micro lending -

7:30 am - Start for Tumkur

10:00 am - Reach the settlement where Grameen Koota (GK) was meeting with the clients (neighbourhood women)

The village joint liability group

10:00-12:00 - Interact with the GK's clients - a Joint liability group in Tumkur

a. GK was doing great, but the loans don't cover their need. Any meaningful investment needed more principal coverage

b. GK should help with health insurance/access to health facilities (local govt. issued health cards giving access to free/cheap medical facility)

c. They need more help on manning their investment/business, to make the loans more useful

- We got see how GK has been organizing the group's borrowings on a simple Loan schedule heet (pic below) - one for each family . the sheet itself is a page from the mifos software, that needs to be extremely simple to make it clear to the client

- How despite the regular payments and availability of the loan, the women still needed to borrow emergency funds (fairly frequently)

- We got to do a Q&A. Interesting observations. The women, all of them, felt :

a. GK was doing great, but the loans don't cover their need. Any meaningful investment needed more principal coverage

b. GK should help with health insurance/access to health facilities (local govt. issued health cards giving access to free/cheap medical facility)

c. They need more help on manning their investment/business, to make the loans more useful

Family card - print from Mifos |  Loan schedule - print from Mifos |

12:00-1:00 - GK branch visit

> There were fairly substantial wads of money lying in the open that the branch manager was individually counting and handing out the loans. An atmosphere of trust and familiarity was palpable

> We found a throng of people sitting outside the branch. We enquired to find, they have all been intimated with a ticket/token number, that their loans have been granted, and are awaiting disbursal for half a day

> We got to know how the loan approval(MFI submits to Credit bureau (CRA like SIBIL, Equifax, HighMark) and disbursement works, and why that may take couple of weeks. That probably explained the crowd gathered outside that were spending a good part of the day sitting idly while they could be earning their $2. Though the MFI officers were doing their best, the process may have more scope to streamline -

Data sent offline --->Then there is check with other MFIs to see if the same party has other loans (total exposure) ---> There is a waiting period to ensure there isn't a parallel application ---> loan approved ---> data sent offline ---> the system has some checks ---> The Client is sent word ---> Client lands up ---> If the system checks are all complete by then, the client gets the money).

> There were fairly substantial wads of money lying in the open that the branch manager was individually counting and handing out the loans. An atmosphere of trust and familiarity was palpable

> We found a throng of people sitting outside the branch. We enquired to find, they have all been intimated with a ticket/token number, that their loans have been granted, and are awaiting disbursal for half a day

> We got to know how the loan approval(MFI submits to Credit bureau (CRA like SIBIL, Equifax, HighMark) and disbursement works, and why that may take couple of weeks. That probably explained the crowd gathered outside that were spending a good part of the day sitting idly while they could be earning their $2. Though the MFI officers were doing their best, the process may have more scope to streamline -

Data sent offline --->Then there is check with other MFIs to see if the same party has other loans (total exposure) ---> There is a waiting period to ensure there isn't a parallel application ---> loan approved ---> data sent offline ---> the system has some checks ---> The Client is sent word ---> Client lands up ---> If the system checks are all complete by then, the client gets the money).

Six principles of (MFI) client protection

1:30-2:30 Nirantara regional office

> A house that doubles up as the office, with couple of furniture and cabinets thrown in

> These guys have a great motto (see picture)

> A house that doubles up as the office, with couple of furniture and cabinets thrown in

> These guys have a great motto (see picture)

The future of Mifos (through our looking glass)

The problem...

1. Micro Finance has received a good pinch of reality since its heydays, causing a glut in contributions from the developer community. While there has been a sobering realization in the developmental world that the backlash as probably extreme and there are definite and comparable benefits to giving the poor better access to financial products, this hasn't yet seen a revival in tech support.

...the opportunity

1. If we we get interested in this space, this probably gives us a chance to get back to contributing to it

The problem...

2. COSM is probably resource constrained leaving a mammoth platform in the hands of insufficient experience and resources

...the opportunity

2. With a clean slate one should stand a good chance of effecting a lot of beneficial influence

The problem...

3. The current platform is obsolete and the design/architecture/roadmap of the new platform is in its infancy

...the opportunity

3. One has a chance to architect the new platform to be much better than the past one

Conclusion

Micro finance has surely come a long way since Muhammad Yunus conceived it and institutionalized it more than thirty years ago. There are, now, a lot more organizations, funding, infrastructure, data, criticism and beneficiaries. This field has also matured as a business model, managing to accomodate professional parties that come together to create value profitably. It is probably on the verge of going past the hype cycle trough, and aims to get into a continuously useful phase. Yet, there is a lot left to be done (more than half the three billion Maries to be reached). A lot of scope for well-intentioned visionary zeal to innovate and discover greater value at the bottom of the pyramid!

RSS Feed

RSS Feed